Loan officials giving financial report mortgage loans need certainly to assemble the bank comments from their buyers after which brush as a result of each one of these, itemizing in more detail new dumps and you may costs to make the journey to good credible money matter

A long time ago, really American homebuyers got normal operate with normal companies that personal loan companies New Castle VA paid them each week or 14 days having regular paychecks. Not any longer. For the past fifteen 2 decades, America’s staff and you can a position patterns provides gone through high transform.

Now, huge numbers of people all over all of the conceivable business work with by themselves while the self-functioning masters, package pros, business owners and you can small enterprises. Because the reasons for meeting themselves differ somewhat, he has got anything in common: most are struggling to qualify for a classic home loan.

New government mortgage tools – Federal national mortgage association and you may Freddie Mac computer (brand new Companies) and you will FHA – fuels the medical and you may well-getting of the You.S. mortgage industry by the guaranteeing brand new flow of funding in order to lenders. When lenders originate mortgages, Fannie, Freddie otherwise FHA buys otherwise promises all of them. The newest finance are up coming securitized and you will offered to traders.

In order to meet more restrictive underwriting requirements appropriate on the Businesses, Freddie and you can Fannie put stricter conditions on the borrower’s mortgage distribution. One particular requirement is actually individuals need to make a manager provided W2 tax setting or government taxation statements to possess guaranteeing earnings. That is problems when you find yourself care about-operating. No W2 hence no qualifying for a classic loan.

In and around 2012, a new types of financial seller came up providing Low-Company money: finance originated beyond your government’s financial structure which aren’t backed by Freddie Mac, Federal national mortgage association otherwise FHA. Deephaven Financial was an early on pioneer in Low-Service finance (often referred to as Non-QM money, QM status to have qualified home loan). If you’re Deephaven even offers a number of different mortgage apps, perhaps one of the most well-known is actually their Financial Declaration finance. These types of finance have fun with a beneficial borrowers’ company otherwise personal checking account statements instead of a W2 to confirm the borrower’s earnings and view their ability to repay the mortgage.

By the examining both the form of home business together with flow away from finance for the and you may out of the borrower’s bank account over a-flat time, generally twelve so you can a couple of years, loan providers can influence: a) the newest borrower’s power to pay the mortgage and b) the correct terms of the mortgage and full amount borrowed, loan-to-really worth proportion, the amount of brand new deposit, and you can any money reserves needs.

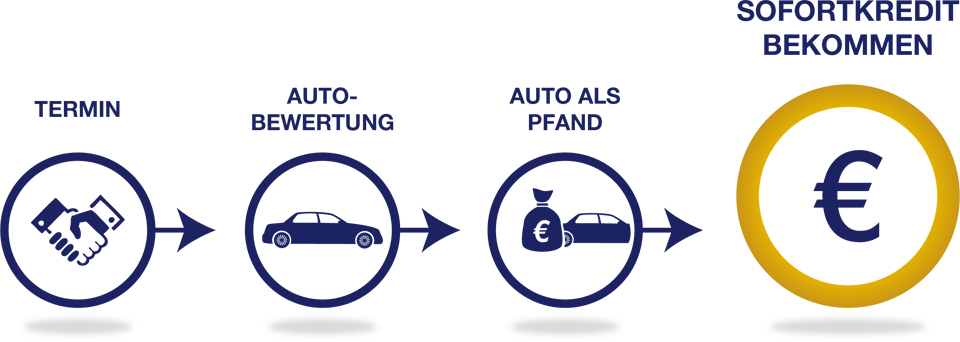

How come a financial statement loan application process functions? Its very simple. The loan manager or agent improving the borrower into home loan uploads brand new several-two years regarding borrower lender comments with the lender’s mortgage processing system. The new lender’s underwriters then use the lender statements to search for the borrower’s normal net gain and you will whether it are adequate to help with the mortgage. Underwriters of bank report mortgages will get to change the fresh terms of the latest loan according to the borrower’s income, debt obligations such student education loans, and you will FICO rating.

A lender Declaration financing are often used to see a primary house, second home, money spent, otherwise any type of mortgage secure from the a domestic a residential property house, along with an effective refinance

You need to note that financial report software may vary in one Non-Company vendor to the next. Most of the time, restriction loan number, loan-to-really worth percentages and FICO ranges are usually uniform all over loan providers. So can be products. Expanded-Prime is actually for consumers one peak lower than prime and you may Non-Perfect is for individuals with often a limited credit score otherwise that are rebuilding their credit. That major differences one of Non-Agencies mortgage providers lies in just who work the brand new underwriting. Financial enterprises such Deephaven Home loan keeps their unique into the-household underwriting professionals and they are for this reason significantly more versatile when it comes so you’re able to common sense s that can help consumers be eligible for their mortgage.

A unique change is the app feel itself. Which have Deephaven Financial, most of the financing officer has to manage are upload the bank statements so you’re able to an online Lender Statement Research tool one to instantly calculates the latest borrower’s normal cash flow and you can income. This conserves the mortgage administrator circumstances off painstaking functions and assists facilitate the entire process of bringing of software in order to underwriting.

That’s all. Now it’s time a basic comprehension of bank declaration home loan applications and exactly how Deephaven is dedicated to supporting their homeownership desires with in and you will great provider. If you are one of the many Us americans which will not discover an effective W2 and you will desires to get yourself started to buy a unique domestic (otherwise refinancing usually the one you are in now), reach out to that loan manager at the regional independent financial team otherwise lender and inquire when they offer Non-Company funds. They’re going to understand what you are speaking of. Now, therefore do you actually.