rwashington

- Texts

A knowledgeable

Having rising cost of living into refuse and hope interesting rates decreasing into the 2024, this new housing marketplace you are going to beginning to warm up again.

- Text messages

- Printing Copy article hook

For the 2023, first-day homebuyers illustrated half of the home orders, accounts home program Zillow. One amount is the large due to the fact Zillow first started staying tabs right back when you look at the 2018 or over about lowest of 37% inside 2021. Of a lot repeat buyers remain on the new sidelines considering the rates secure perception, that’s in which residents is actually incentivized in which to stay the most recent homes for their low mortgage rates of interest. However with inflation towards the decline additionally the guarantee of great interest cost decreasing in 2024, new housing market you certainly will begin to warm up once again.

Affording a house was a difficult hill in order to go, and installment loans in South Carolina it is specifically high for these buying their earliest family, Zillow Elder Economist Orphe Divounguy states. Headwinds like mortgage pricing, lower inventory, and you can ascending rents continue to be strong however, easing. Attractive land try moving timely, so people looking to buy which spring need to have their earnings manageable today, including taking pre-approved to have home financing. The rise inside the the fresh listings which springtime, owed one another to this new design and also to more property owners choosing to promote, gives customers much more possibilities which help ease price development. The latest homes teach are delaying sufficient supply a whole lot more first-time people a way to hop on board.

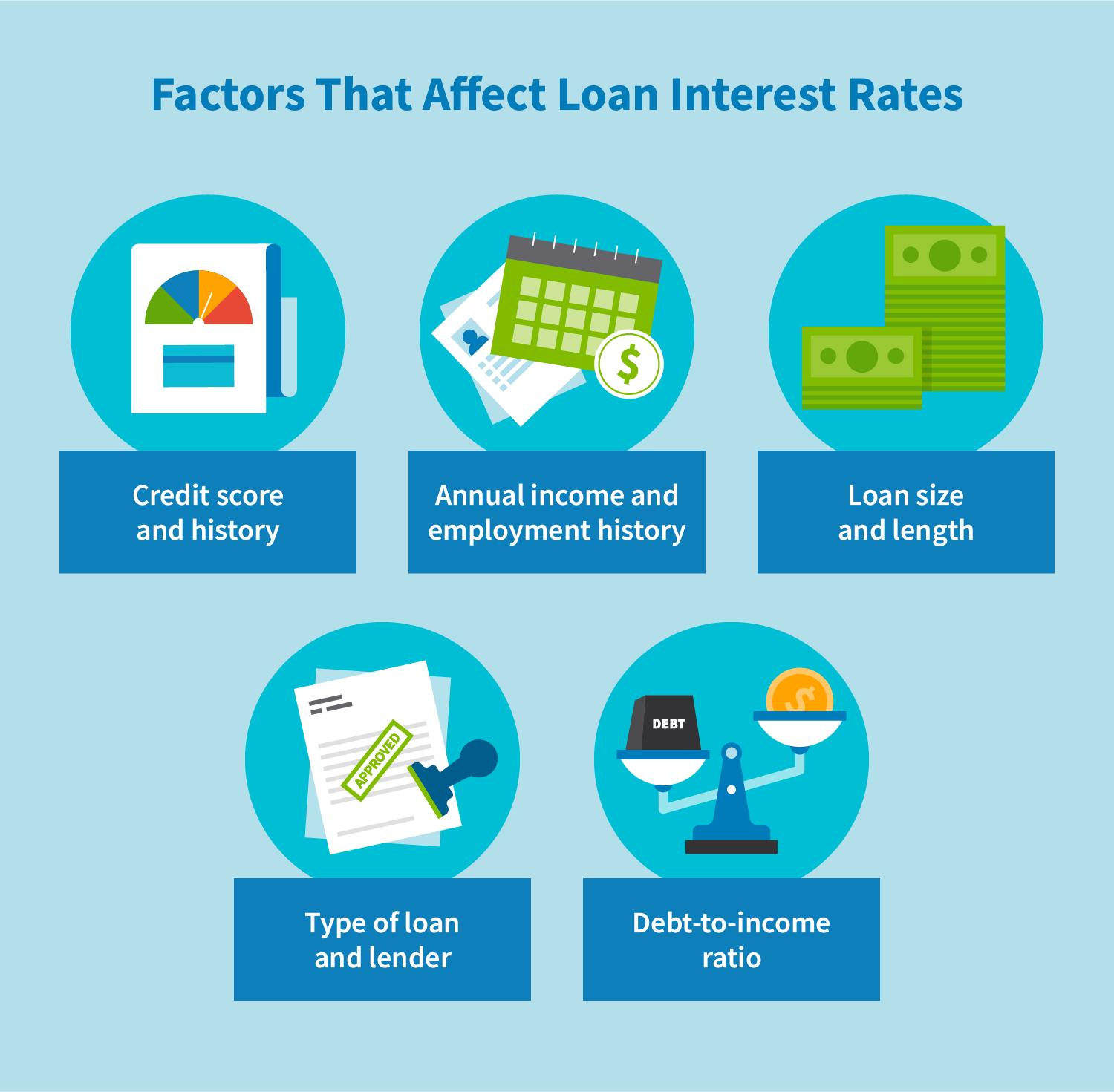

Experts used several different metrics to rank this type of very-max segments – the fresh new share out of to possess-business postings the common house is also easily pay for, expected competition, as well as the number of furthermore-old homes close. To choose the average household’s value, the newest declaration put aren’t quoted national averages – 30% off month-to-month income into home financing, a beneficial 5% down-payment, and six.94% home loan interest. Nonetheless they checked out the brand new ratio out-of affordable to possess-product sales index in order to occupant house, much more availability for each tenant house ways faster consumer battle.

St. Louis, Missouri, and Detroit, Michigan, topped this new affordable field listing. Both metros boast increased rental cost, giving affordable property and you will enabling customers to bulk right up their discounts. Without listed as among the cheapest ong locations with furthermore-old houses.

Zillow’s online tools give potential earliest-go out consumers guidelines to make new homeownership dive out-of economic maturity to help you agent choice. On top of that, they provide an enthusiastic cost calculator people are able to use so you can tabulate their budget. Which calculator and facts in some of the homeownership’s invisible costs.

Looking for an excellent mortgage officer can help housing marketplace newbies understand its solutions to discover whether or not a changeable rate financial or paying facts most useful benefit for every consumer’s book financial predicament. So you can lift credit scores, clients spending landlords as a consequence of Zillow can be opt on the rent fee revealing, that will report about-date book repayments to a primary national borrowing agency.

In spite of the process’ a lot of, commonly frustrating hurdles, down repayments are nevertheless a high question certainly earliest-time buyers. Individuals who have not protected sufficient to have good 20% down-payment do not need to care and attention, because the up to 50 % of customers eventually set out lower than 20%. On the other hand, Zillow now offers pages use of down-payment direction apps that will affect certain listings.

Unique reasonable mortgages, bodies stimulus apps, and money offers and bonuses will help being qualified very first-big date people reach homeownership. The borrowed funds financing system HomeReady, contributed from the Fannie mae, helps legitimate, lower-income buyers to make down money. People using the services normally set as low as step 3% down that have to own quicker home loan prices and lower financing can cost you. HomeReady constraints can be found, however, unqualified customers can always slim into the almost every other comparable applications.

Dollars features is actually low-repayable gift suggestions to aid the brand new people make their first pick. The new low-finances organization, The fresh new Federal Homebuyers Loans, provide very first-timers having a grant as high as 5% of their possible home’s price. The fresh finance enjoys contributed doing $460 mil into the deposit assistance because 2002, providing an estimated 52,000 houses put down roots. Buyers never directly realize so it offer; simply mortgage businesses can apply.

Government stimulus applications can also be found so you’re able to very first-day customers. The initial-Day Homebuyer Act away from 2024 provides eligible buyers a federal tax borrowing from the bank of up to $fifteen,000, which will surely help customers create down money. Modeled adopting the Obama Basic-Go out Visitors Income tax Borrowing from the bank, it can be called the Biden Very first-Time Visitors Tax Borrowing from the bank pursuing the Biden administration’s force to include good-sized affordable construction.